What Is a Review Audit? A Guide for Business Owners

What Is a Review Audit? A Guide for Business Owners

TL;DR:

- A review audit provides limited financial assurance through inquiry and analytical procedures, not detailed testing.

- It is a cost-effective and faster option for small businesses needing professional verification without a full audit.

A review audit is an independent financial assessment that delivers limited assurance on financial statements through inquiry and analytical procedures, without the full scope of a traditional audit’s detailed transaction testing. The formal industry term is a “review engagement,” governed by the International Standard on Review Engagements (ISRE 2400). Business owners in local markets often encounter this requirement when lenders, investors, or regulators need professional verification of financial health, but a full audit is either too costly or not legally required. This article explains what a review audit involves, how it differs from a full audit, and why it may be the most practical credibility tool available to you.

What is a review audit, and how does it differ from a full audit?

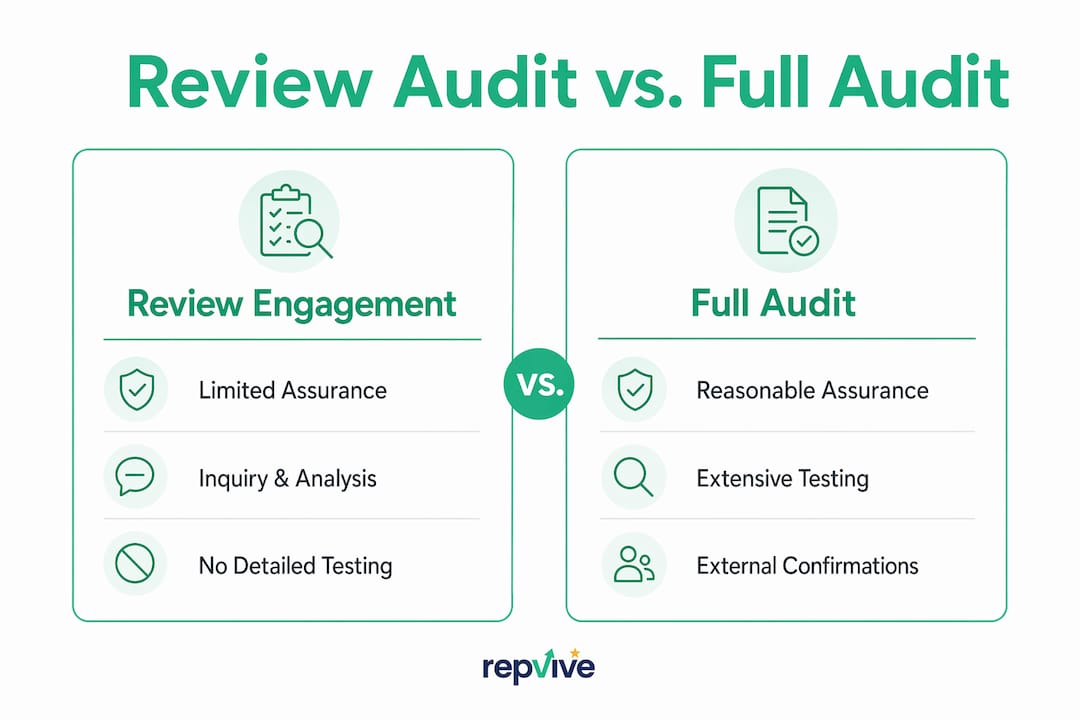

A review audit, formally called a review engagement, sits between a compilation and a full audit on the assurance spectrum. A compilation provides no assurance, a review provides limited assurance, and a full audit provides reasonable assurance. That distinction matters because it determines how much confidence a lender, investor, or regulator can place in your financial statements.

The core difference lies in what a CPA actually does during each engagement. A full audit includes detailed transaction testing, physical inventory counts, and external confirmations from banks and customers. A review engagement relies primarily on two procedures: inquiry of management and analytical procedures. The CPA asks targeted questions about your financials and analyzes trends, ratios, and comparisons to spot anything that looks unusual.

The conclusion language also differs. A full audit concludes that financial statements are presented fairly. A review engagement concludes using “negative assurance,” meaning nothing came to the CPA’s attention that required material modification. That phrasing is not a weakness. It is a precise professional statement that reflects the scope of work performed.

| Feature | Review engagement | Full audit |

|---|---|---|

| Assurance level | Limited (negative assurance) | Reasonable (positive assurance) |

| Primary procedures | Inquiry and analytical review | Transaction testing, confirmations |

| External confirmations | Only if anomalies arise | Standard requirement |

| Typical cost range | $8,000–$25,000 | Significantly higher |

| Typical timeline | 4–6 weeks | Several months |

| Best suited for | SMBs, lenders, some regulators | Public companies, legal mandates |

Pro Tip: If a lender asks for “reviewed financials,” they are requesting a review engagement, not a full audit. Confirm the exact requirement in writing before engaging a CPA to avoid paying for more assurance than the situation demands.

How to conduct a review audit: key steps and best practices

Conducting a review audit follows a defined process under ISRE 2400. The steps are sequential, and skipping any one of them creates professional and legal risk for the CPA and credibility risk for you.

-

Understand the entity. The CPA starts by learning your business model, industry, accounting policies, and any changes from prior periods. This context shapes every inquiry and analytical procedure that follows.

-

Set materiality thresholds. Materiality is typically set at 1–5% of revenue. This threshold determines which discrepancies are significant enough to investigate further. Setting it too high misses real problems; setting it too low creates unnecessary work.

-

Perform inquiries of management. The CPA asks structured questions about revenue recognition, expense categorization, related-party transactions, and any significant accounting judgments. Your answers become part of the documented evidence.

-

Apply analytical procedures. The CPA compares current period figures to prior periods, budgets, and industry benchmarks. Unusual fluctuations trigger follow-up questions or additional procedures.

-

Evaluate findings and escalate when needed. ISRE 2400 requires conditional escalation: if analytical procedures reveal anomalies, the CPA must perform additional targeted procedures before issuing any conclusion. This step is non-negotiable under professional standards.

-

Prepare the review report. The CPA documents all procedures, findings, and conclusions. The final report uses negative assurance language and is addressed to the appropriate party, typically management or the board.

-

Deliver and communicate results. The CPA presents the report and discusses any findings with you. If material issues surfaced during the engagement, those require resolution before the report is finalized.

Pro Tip: The most common failure point in review engagements is skipping conditional escalation. If your CPA identifies an unusual fluctuation but does not perform additional procedures before concluding, the engagement does not meet ISRE 2400 standards. Ask your CPA directly how they handle anomalies during the analytical phase.

What are the benefits of review audits for business owners?

Review audits deliver real, practical value beyond satisfying a regulatory checkbox. For local business owners, the benefits show up in three areas: credibility, cost efficiency, and early problem detection.

Review audits build credibility with lenders and investors by providing professional verification of financial health without full audit costs. That means a bank reviewing your loan application sees independently reviewed financials, which carries significantly more weight than self-prepared statements. The same applies to potential investors or business partners evaluating whether to work with you.

The cost and time advantage is concrete. Review engagements typically cost between $8,000 and $25,000 and take 4–6 weeks to complete. Full audits run considerably longer and cost more, often by a factor of two or three. For a small or mid-sized local business, that difference is significant.

The benefits in summary:

- Stakeholder confidence. Lenders, investors, and regulators treat reviewed financials as professionally verified, which strengthens your negotiating position.

- Early issue detection. Analytical procedures often surface inconsistencies that internal teams miss, giving you time to address problems before they escalate.

- Compliance support. Some loan covenants, grant agreements, and industry regulations require reviewed financials rather than a full audit. A review engagement satisfies those requirements at lower cost.

- Reputation for transparency. Voluntarily obtaining a review engagement signals financial discipline to stakeholders, even when it is not legally required.

- Faster turnaround. The 4–6 week timeline means you get professional verification without waiting months for a full audit cycle to complete.

Business owners should view review audits as proactive tools that build credibility beyond mere compliance. The businesses that use them strategically, rather than reactively, tend to have stronger relationships with their financial stakeholders.

Common misconceptions about review audits

The biggest misconception is that a review audit is simply a cheaper, less thorough version of a full audit. That framing is wrong. A review engagement is a distinct professional engagement with different objectives, different procedures, and a different form of conclusion. Treating it as a “lite audit” misunderstands both what it delivers and what it cannot deliver.

A second common misunderstanding involves independence. A CPA cannot perform both an audit and a review engagement for the same client during the same reporting period. This rule exists to prevent conflicts of interest between assurance engagements. If your current audit firm also offers review services, they cannot provide both for the same period.

Other points business owners frequently overlook:

- Conditional escalation is mandatory, not optional. ISRE 2400.52 requires additional procedures when anomalies appear. Many practitioners skip this step, which compromises the engagement’s validity.

- Negative assurance is not weak assurance. The phrasing reflects the scope of the engagement, not a lack of rigor. Stakeholders familiar with professional standards understand this distinction.

- Legal obligations vary by jurisdiction. Some industries and loan agreements specify which engagement type is required. Assuming a review will satisfy a requirement that mandates an audit creates legal and financial risk.

- Choosing the wrong engagement type is costly. Completing a review when stakeholders needed an audit means starting over, paying twice, and losing time.

Pro Tip: Before engaging any CPA, consult your lenders, investors, and any relevant regulators to confirm exactly which engagement type they require. Early stakeholder coordination prevents expensive mistakes and ensures the assurance you obtain actually satisfies the needs of the people relying on it.

Key Takeaways

A review audit is a distinct professional engagement that provides limited assurance through inquiry and analytical procedures, making it the most cost-effective credibility tool for local business owners who need professional financial verification without a full audit.

| Point | Details |

|---|---|

| Definition of a review audit | A review engagement provides limited assurance using inquiry and analytical procedures, not detailed transaction testing. |

| Cost and timeline advantage | Review engagements typically cost $8,000–$25,000 and complete in 4–6 weeks, far faster than a full audit. |

| Conditional escalation is required | ISRE 2400 mandates additional procedures when anomalies arise; skipping this step invalidates the engagement. |

| Independence rules apply | A CPA cannot perform both an audit and a review for the same client in the same reporting period. |

| Strategic credibility tool | Reviewed financials strengthen your position with lenders, investors, and regulators beyond mere compliance. |

Why I think most local business owners underestimate review audits

Most local business owners I speak with treat a review audit as a bureaucratic hurdle, something a lender asked for and they need to check off a list. That framing costs them real opportunity.

The businesses that get the most value from review engagements use them proactively. They obtain reviewed financials before approaching a lender, not after the lender asks. They use the analytical procedures as an internal diagnostic, not just a document to hand over. When a CPA’s inquiry surfaces an inconsistency in revenue recognition or an unusual expense trend, that is genuinely useful information, not a problem to manage.

The credibility signal also compounds over time. A business that presents reviewed financials consistently, year after year, builds a track record of transparency with its banking relationships. That track record has real value when you need a line of credit extended or a loan restructured quickly.

The same logic applies to your online reputation. Financial transparency and public trust reinforce each other. A business with clean, reviewed financials and a strong online reputation is a fundamentally more credible operation in the eyes of every stakeholder that matters. Treating either one as a checkbox exercise misses the point entirely.

— Jason

How Repvive helps protect the reputation your review audit supports

A review audit builds financial credibility. Your online reputation either reinforces or undermines that credibility with every potential customer who searches for your business.

Repvive’s attorney-led review removal service addresses fake and unfair Google reviews that damage the trust you have worked to build. With a 99% success rate and no upfront fees, Repvive crafts customized legal claims for each review and works directly with Google to get removals approved. You can also start with a free Google Business Profile audit to see exactly where your online reputation stands right now. Financial credibility and online reputation belong in the same conversation.

FAQ

What is a review audit in simple terms?

A review audit, formally called a review engagement, is an independent assessment where a CPA analyzes your financial statements using inquiry and analytical procedures to provide limited assurance that nothing requires material modification.

How long does a review audit take?

Review engagements typically take 4–6 weeks to complete, depending on the complexity of the business and the responsiveness of management during the inquiry process.

What is the difference between a review audit and a full audit?

A full audit provides reasonable assurance through detailed transaction testing and external confirmations. A review engagement provides limited assurance through inquiry and analytical procedures only, at lower cost and in less time.

What does ISRE 2400 require during a review engagement?

ISRE 2400 requires the CPA to perform additional targeted procedures whenever analytical procedures reveal unusual fluctuations or anomalies, before issuing any final conclusion on the financial statements.

Can the same CPA firm perform both an audit and a review for my business?

No. Independence standards prohibit a CPA from performing both an audit and a review engagement for the same client during the same reporting period, as this creates a conflict of interest between assurance engagements.